COPART: THE ENDLESS COMPOUNDING MACHINE

Strong revenue growth, stable relationships with insurers, increasing gross margin, prudent financing, consistent high returns on capital and effective capital allocation.

Hi there, welcome back to AG Quality Capital! As always, we're diving into the world of long-term quality investing in the stock market.

This is my first Deep Dive for the blog, and it focuses on one of the companies that has captured my attention the most: Copart. In this analysis, you will find:

BUSINESS MODEL

COMPETITIVE ADVANTAGES

INDUSTRY DRIVERS

INDUSTRY STRUCTURE AND COMPETITIVE POSITION

REINVESTMENT OPPORTUNITIES

FINANCIALS

MANAGEMENT AND COMPENSATION STRUCTURE

RISKS

HOW COPART FITS MY TRAIT

Let’s go for it.

1. THE BUSINESS:

What the Company Does:

Copart is a leading provider of online auctions and vehicle remarketing services with operations in several countries around the world. The company offers sellers a range of services to process and sell cars online through an auction-style sales technology called VB3. According to the company's website, it currently has over 350,000 vehicles available for sale.

The primary source for its fleet supply comes from insurance companies that declare a vehicle a total loss after an accident.If the repair costs exceed the difference between the vehicle's value before the accident and the amount the insurer can obtain by auctioning it, the insurer will decide to declare it a total loss.

For example, if the value of the vehicle before the accident is $14,000 and repairing it costs $10,000, but the insurer would receive $5,000 if it is auctioned, the option chosen will be to declare it a total loss, as it results in a smaller loss ($9,000 loss if totaled versus $10,000 loss if repaired).

Insurance companies consider Copart to be a very attractive option due to the economic planning it represents for their business. The company helps insurers determine the value they can obtain from the auction through software it has refined over the years called Proquote. This software has been developed with data collected from its experience in the industry. It requires a fairly high level of complexity for calculations, as it includes data such as brand, model, auction steps of the vehicle, nature, severity of damage, among others. Through this software, insurers can make better business plans and become more efficient in managing their vehicles.

It also proves to be attractive for insurers during extraordinary events like hurricanes, which can damage many cars at the same time, so they leverage Copart's scale to assist in the contingency. While this translates to additional costs for the company in the short term due to leasing temporary facilities, labor, and overtime hours, it also represents a very important value-added service for insurers, who are its primary clients and account for over 80% of the market volume.

How Copart makes money

Service Revenue: This consists of fees related to auctions charged for vehicle remarketing services. This can be based on a percentage of the vehicle's sale price or a fixed fee. There are also fees for transportation, processing, storage, bidding and vehicle loading. These revenues have accounted for over 85% of the total for the past six years.

Vehicle Sales Revenue: The company also purchases vehicles and resells them in its own name. Revenues from this part of the business include the gross sale price and have represented the remaining 15% in recent years.

Advantages of the Business Model:

Copart's business model has several advantages, which are highlighted below:

It increases the pool of buyers interested in a vehicle by eliminating the inconvenience of having to attend a live auction. This creates greater competition for bids and results in a higher final acquisition price, which is more advantageous for the seller.

In the United States and Canada, it provides its own transportation services through a combination of third-party companies and a fleet of over 140 vehicles. This allows them to pick up most cars from sellers within a maximum of 24 hours.

Copart provides sellers with real-time data on the vehicles they process, which includes gross and net returns for each sale, service charges, and other data that allow them to manage and monitor the entire process.

2. COMPETITIVE ADVANTAGES:

Barriers to Entry:

The competitive advantage from barriers to entry comes from several fronts:

Difficulty in Acquiring Land: Acquiring land for vehicle storage presents a significant regulatory barrier, as permits are required that can take a long time to obtain, given that vehicles can leak hazardous materials and chemicals into the ground. Copart benefits from what is commonly known as NIMBY (Not In My Backyard); no one wants a junkyard around the corner, and essentially, anyone wanting to acquire land for Copart would need to buy it from them.

Many years ago, management recognized the enormous potential in the industry and, instead of leasing land, they began purchasing it. As cities expanded, they found that their junk storage lots were getting closer to urban areas, giving them not just the asset but a cost advantage as well.

Necessary Investment: Copart owns lots totaling over 17,000 acres and can collect more than 250,000 vehicles per month, with a maximum pickup time of one day. While the costs of acquiring land vary depending on location and macroeconomic factors, it is known that obtaining something similar entails a significant capital outlay.

For example, during one of the 2017 earnings reports, management mentioned that the cost per acre in Miami was over $1 million and shortly thereafter rose to $1.2 million; in South Bay, San Francisco, it was $1.7 million per acre. This not only is expensive but also creates planning issues for new entrants to the market.

Relationship with Insurers: In recent years, revenue from insurers has accounted for over 85% of the total and represents 80% of the market volume. For a new competitor to enter the market, insurers would need to see a liquidity network similar to that of Copart; otherwise, it would not make sense for them to build a relationship with a new competitor.

Essentially, they will prefer the option that offers higher bidding prices, which requires a flow of buyers and sellers similar to that of Copart. Furthermore, A new entrant cannot support the creation of a network connecting buyers and sellers until they have the cars, which simply cannot happen until they have the land—something that, as we’ve seen, has significant regulatory and capital barriers.

Network Effect:

Copart leverages network effects through the auction technology it offers users. This has benefited from the continuous growth in the available vehicle supply, which currently exceeds 350,000 units ready for sale, and will likely continue to increase as they acquire more land for additional storage capacity.

From the consumer side, it is natural for users to be more attracted to a platform with a larger available supply, which in turn increases user demand for auctions and allows for higher prices for sellers. Essentially, sellers will want to go where they can get a better sale price, and buyers will choose the site with the most options available.

Economies of Scale:

Copart has over 200 dismantling facilities located in the United States and other countries where it operates. As this number has increased, they have achieved economies of scale, reducing transportation costs and improving pickup times for each incremental dismantling facility within the same region. With these cost reductions, the company has achieved savings over the years that have allowed it to acquire additional land.

3. INDUSTRY DRIVERS:

The market in which Copart operates is influenced by several key factors:

Increase in Total Loss Rate: Copart’s business has naturally benefited from the increase in the total loss rate of vehicles, which has risen from 4% in 1980 to 20% in recent years. This is mainly due to the rising costs of vehicle repairs, making it more likely for insurers to declare a vehicle as a total loss. The following factors have contributed to the increase in repair costs:

Vehicle Complexity: The current composition of vehicles has made repairs increasingly expensive. The growing complexity of parts, due to the large number of cameras, sensors, and other technologies, has driven up prices, increasing the cost of repairs. It is estimated that these parts have grown at rates exceeding 10% over the past 20 years.

Market Consolidation: The auto repair industry is consolidating, and as it becomes more of an oligopoly, there is very little price competition, allowing companies to charge significant premiums for their services. At the same time, cars are becoming more complex, requiring more skilled labor, which consequently charges more for its services. All of this contributes to higher repair costs, which in turn increases the total loss rate.

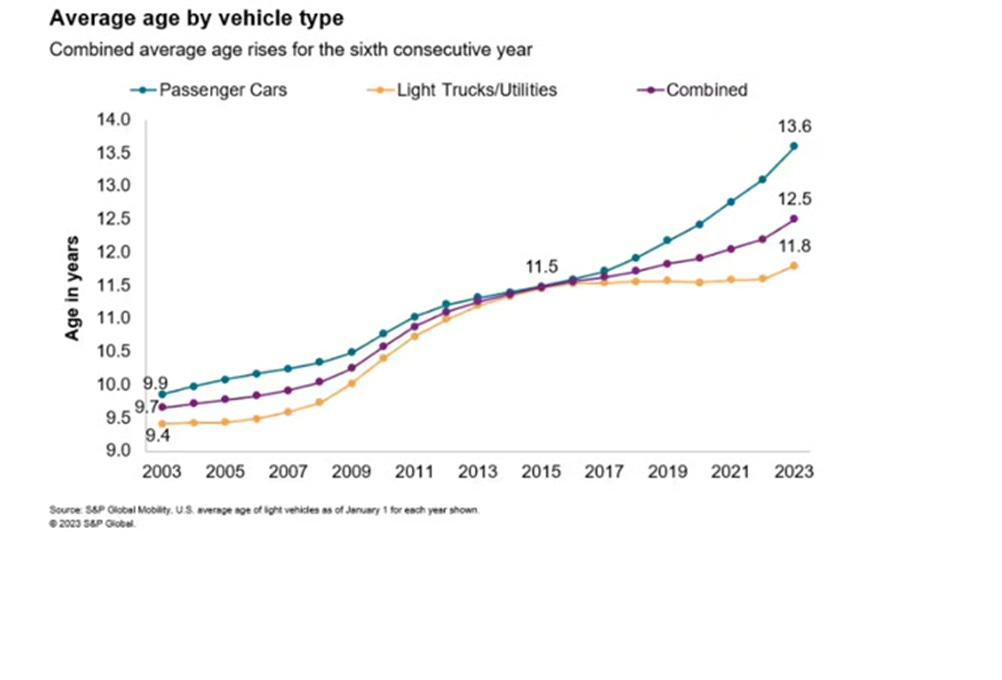

Vehicle Fleet Age: The average age of vehicles reached an all-time high in the latest report from March 2023, continuing an upward trend that has extended over the past two decades.

With over 284 million vehicles on the roads in the U.S., the average age of cars and trucks has increased again to 12.5 years. The fact that the vehicle fleet is trending this way also benefits Copart’s business due to the total loss equation: As vehicles age, their pre-accident value decreases, increasing the likelihood that they will be declared a total loss.

Used Car Prices: Initially, it might seem logical to think that Copart's business is heavily dependent on used car prices; however, management has always maintained a neutral stance on this issue.

In general, higher used car prices result in better unit economics for Copart, meaning they make more money on the cars that are sold, but they also handle fewer units due to the total loss equation. Lower used car prices mean they face less attractive unit economics, but they would sell many more units.

4. INDUSTRY STRUCTURE AND COMPETITIVE POSITION.

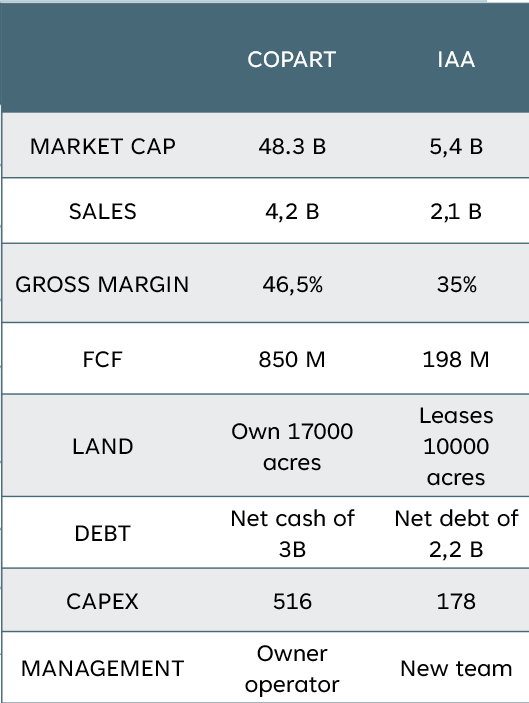

It is estimated that Copart controls 50% of the market, and together with its main competitor (IAA), they hold an 80% market share. The salvage car industry is essentially dominated by these two players, but even between them, there are significant differences.

Copart is clearly the best company in the industry, and this success is a result of superior management. While Copart has always had a management team motivated by long-term growth, IAA has seen its leaders focus on generating short-term profits.

Years ago, IAA was even better positioned in the industry. It was the first in the sector to go public and seemed poised to win the race; however, it was Copart that decided to play the long game, recognizing early on that land ownership could be the key differentiator in the long run. While Copart chose to acquire land, IAA opted to lease it.

There is also a significant difference in how they invest in technology. Copart has never hesitated to spend on improving the customer experience with their online auctions, something that IAA only managed to implement during the COVID pandemic.

The differences between the two companies are very clear today. Copart generates twice the sales, has substantially higher margins due to its cost advantage, boasts a free cash flow (FCF) that is 4.5 times greater for reinvestment, owns crucial land assets, carries no debt on its balance sheet, and is managed by a top-tier management team.

5. REINVESTMENT OPPORTUNITIES

Copart's reinvestment opportunities are driven by its core business in both local and international markets. Copart does not need to expand into other business lines or make acquisitions to continue growing.

Europe seems to be a logical market for expansion, with a vehicle fleet size similar to that of the United States. Similarly, China presents another significant opportunity, with a large number of vehicles, although Copart's presence there is still quite limited.

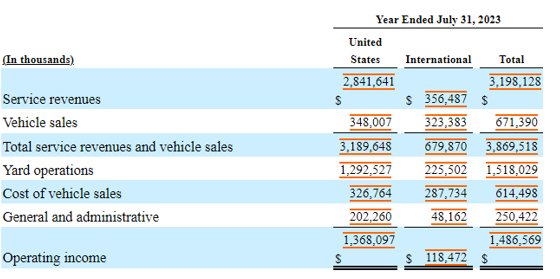

The previous table represents the results obtained in the last fiscal year for the United States and other countries. It highlights a significant difference between these regions that is important to note:

Service Segment Sales: The service segment sells 8 times more in the United States than in other countries. Copart has been able to successfully implement its business model in the U.S., proving its effectiveness over the years. However, in international markets, the company has yet to develop to its full potential, despite these markets being similar to the American one.

Management has mentioned in recent earnings reports that they have been investing in infrastructure to achieve greater scale in the long term. As the company invests in lots for vehicle storage, a virtuous cycle similar to the one in America will form, where increased storage capacity attracts more demand, which in turn brings more supply, as better auction prices can be obtained. This will further enhance the company's scale, making its operations more efficient.

Operational Margin Differences: In the United States, there is an operational margin of 48%, compared to 33% internationally. These differences arise from two fundamental factors: 1) The stronger economies of scale in the U.S., where investments in storage and transportation have progressively reduced costs as sales have increased, and 2) The business model applied by certain European insurers results in a lower residual value per vehicle, which negatively impacts profit margins.

6. FINANCIALS

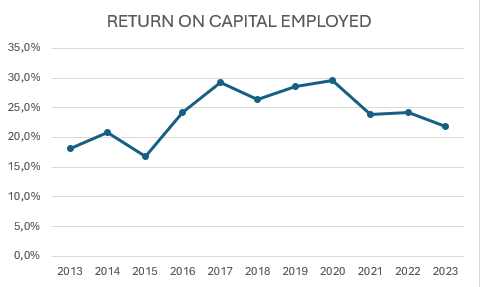

Return on Capital Employed: Copart has achieved returns on capital employed exceeding 20% in recent years. Such consistently high returns are indicative of a company with strong competitive advantages and the ability to generate sustained value for its shareholders.

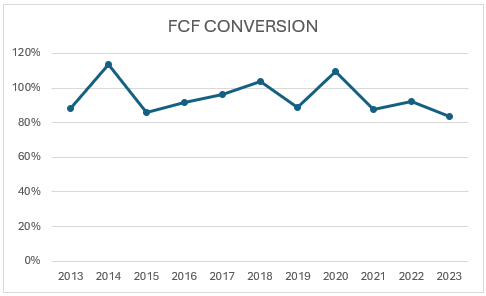

Cash Conversion: Despite being a capital-intensive business, Copart manages to convert a significant portion of its earnings into cash, ensuring that it can use the generated cash for reinvestment in the business. Notably, Copart has historically reinvested its capital in growth, opting not to pay dividends and only repurchasing shares when they are significantly undervalued.

Financing: Copart demonstrates a solid and prudent financial position. The fact that it holds more cash than debt on its balance sheet is a positive indicator that the company is not overly leveraged and can face economic downturns with greater resilience.

Additionally, the consistent generation of cash flow through its operations further reinforces this financial stability. According to its latest balance sheet presented in May 2024, Copart has $3 billion in cash and no debt, allowing it to withstand any potential weakness in demand without issue.

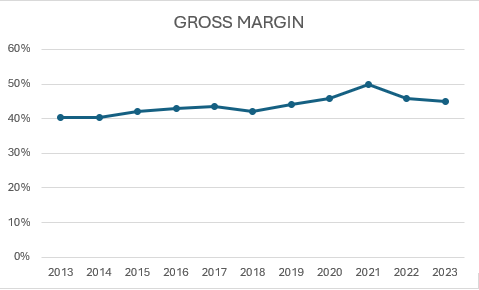

Gross Margin: Copart has seen an increase in its gross margin, driven by the growth in the scale of its operations. Efficiency in process management and cost optimization have contributed to this rise in profitability. Furthermore, the outlook for this trend remains positive, particularly due to its expansion into international markets, which should enable the company to gain even more scale and efficiency.

Sales: Over the past five years, Copart has experienced impressive sales growth, with a compound annual growth rate exceeding 20%. This consistent increase in revenue is a positive indicator of the company’s ability to capture a larger market share and effectively expand its operations.

Capital Allocation: Prudent capital management is a hallmark of Copart. The company maintains a cautious approach to share buybacks, only executing them when the stock trades at attractive multiples. This reflects a mindset focused on generating long-term shareholder value. Additionally, by not paying dividends and reinvesting excess cash back into the business, Copart demonstrates its strategic vision to use capital effectively for growth and expansion.

7. MANAGEMENT AND COMPENSATION STRUCTURE

JAYSON ADAIR (Co-CEO): He is the son-in-law of the company's founder, Willis Johnson, who is currently on the board of directors and still holds 5.82% of the outstanding shares. Adair has been in the role since 2010 and has over 30 years of experience within the company. During his tenure, the stock has multiplied more than 20 times. He owns 3.71% of the company’s shares, which currently represents about $1.8 billion in market value.

Adair does not receive cash compensation in the form of a base salary or annual cash incentives. Instead, he only receives stock options granted at an exercise price equal to the closing sale price of the common stock on the grant date, meaning he can only realize benefits if the stock price increases. This is undoubtedly the type of management that investors like to see in a company; in addition to his experience in the role and strong performance, he has a significant amount of his capital invested there, and the compensation he receives in the future also depends on the stock price.

JEFFREY LIAW: He has been co-CEO since 2022 and previously served as the President for North America in 2021 and as CFO for nearly five years. Although his compensation structure differs from Adair's, a significant portion of it is tied to the company’s operational performance.

Overall, Copart's management, led by Jayson Adair and Jeffrey Liaw, reflects a clear long-term mindset that translates into outstanding results for shareholders. Adair, with over 30 years at the company and a significant equity stake, has demonstrated a strong commitment to sustained growth, aligning his incentives with stock performance. His focus on creating value is complemented by Liaw's experience, who also has his compensation linked to operational performance. This alignment of interests and the accumulated experience in their roles highlight Copart's solid management strategy.

8. RISK FACTORS

The primary long-term risk Copart faces is the adoption of autonomous vehicles, which could significantly reduce road accidents and, consequently, the rate of total loss claims.

When will autonomous vehicles become a reality?

Some studies suggest that by 2030, autonomous vehicles will be reliable enough for widespread use. However, skepticism is warranted due to the numerous challenges still facing their development, costs and benefits. While some vehicles today are being developed with Level 2 or 3 autonomy (requiring human intervention), complete Level 4 vehicles (no human intervention) face hurdles such as adverse weather conditions and unpaved roads. Given these challenges, it will likely take many years of testing and regulatory approval before autonomous vehicles are commonplace.

Early commercial autonomous vehicles are expected to be expensive and limited in performance. Market adoption might take even longer, with projections suggesting that by 2030, autonomous vehicles will be commercialized, but only by 2045 will half of new vehicles be autonomous, and by 2060, half of the global fleet could be autonomous.

How long have previous advancements taken to develop?

Considering how automotive advancements have historically developed can provide perspective on the timeline for autonomous vehicles:

Automatic transmission: Began development in the 1930s, took 50 years to become reliable.

Airbags: Started in the 1970s, became standard by the end of the millennium.

Although these examples may not directly correlate with autonomous vehicles, they highlight the extended timeline often required for major automotive innovations to become widespread. The transition to autonomous vehicles is even more complex and costly, suggesting that market acceptance could take even longer. Additionally, the increasing durability of current vehicles could further delay the turnover to a predominantly autonomous fleet.

Additional risks with implementing an autonomous fleet

Statistics show that 90% of accidents are due to human error, leading to expectations that autonomous vehicles could drastically reduce accidents. However, this conclusion overlooks several important factors:

Operational failures: Complex electronic systems often fail due to distorted signals or software errors, and autonomous vehicles will likely experience failures contributing to accidents.

Increased vehicle usage: Autonomous vehicles may increase total vehicle miles traveled, thereby increasing exposure to accidents.

Risks to non-automobile users: Autonomous vehicles may struggle to detect pedestrians, cyclists, and motorcyclists.

Given these factors, it is unlikely that accident rates would drop by 90% even with widespread autonomous vehicle adoption. Some studies suggest that approximately 34% of accidents could be prevented, meaning that while significant, the reduction in accidents would not be total.

9. HOW COPART FITS MY INVESTMENT TRAIT

Copart possesses many characteristics that align with my investment preferences. This company have yielded a 28.7% CAGR return for its investors over the past 10 years, with no signs of this changing in the future.

Duopoly: The salvage car industry is dominated by two companies, Copart and IAA, which control 80% of the market, with Copart holding approximately 50%. In an industry with such high barriers to entry, it is foreseeable that Copart will continue to be a dominant player.

Growing demand: High repair costs have been a major driver of the industry in recent years and are expected to remain so given the complexity of new vehicles, increasing the likelihood of total loss claims. With a superior network, Copart is well-positioned to capitalize on the growing demand in the industry, providing little reason for buyers and sellers to go elsewhere.

Dominant own networks: Copart has built a dominant network with its land and marketplace. Its strategically located salvage yards provide a cost advantage. Additionally, its network of buyers and sellers offers significant value. A new competitor would need to match this liquidity to attract supply, and without land for vehicle storage, this would be nearly impossible.

Additional controls over competitive supply: Copart has high switching costs for sellers. The value it offers insurers in business planning is difficult to match. Copart has also shown care for its customers during natural disasters with large volumes of damaged vehicles. Simply put, sellers have no reason to seek value elsewhere.

Copart also benefits from NIMBY (Not In My Back Yard), as no one wants a salvage yard nearby, giving Copart a regulatory advantage in preventing new entrants.

Pricing power: Copart can increase prices without losing demand, having spent years enhancing its service value, especially for insurance companies, which are unlikely to resist price changes to better plan their businesses.

Financial aspects: As discussed earlier, Copart’s financials are favorable, with strong returns on capital, high free cash flow conversion and prudent financing.

Management aligned with shareholders: Management has a shareholder-friendly compensation structure, with founders still holding significant stakes in the company and demonstrating a long-term business mindset.

Final words:

As is the case with many high-quality companies, Copart's valuation appears elevated, currently trading at approximately 34 times the estimated free cash flow for fiscal year 2025. While it may not be a bargain, quality investors should keep two key points in mind: 1) A business of this caliber doesn't come around often, and the market has already recognized its true value and 2) When conducting a valuation based solely on next year’s earnings, there's a risk of underestimating the power of compounding over the long term.

Without a doubt, Copart is one of those rare companies with significant competitive advantages that has remained off the radar of the average investor for quite some time. Often deemed "boring" due to its involvement in an unattractive industry, the returns experienced by its shareholders have been anything but dull.

Would you consider Copart in your portfolio? Share your thoughts in the comments and let me know what you think about its long-term potential.